Assessing VC Funds

What to assess when reviewing VC decks

Every man, woman and their dog is raising a fund these days, I’ve returned a decent amount through funds, here’s how to separate the wheat from the chaff

My experience

I’ve deployed actively into funds over the past 3 years, most notably into the funds Upside, Firedrop and Intuition. Sadly I didn’t meet the minimum for Concept’s fund 3 years ago, but will be going into their fund II. At the same time, I’ve passed on dozens of other funds - because most funds don’t perform.

I actively pursue 3 strategies when putting my (micro) cheques into these funds.

Growth funds that can access hot deals. There is a literal two tier world when it comes to funds, with the top ones having the pick of deals on the hottest AI and defence startups that are virtually guaranteed next rounds, and everyone else. If you can get into hot deals in hot funds, do.

I do this through syndicating funds and using creator leverage to get into deals. If you’re interested in accessing these or joining a syndicate, hit me up.Emerging managers: these managers are often hungry and can access deals once the rounds are almost closed by virtue of the value they add relative to ticket size. They are statistically generating better returns and a lot of LPs are super keen to get in.

Creator economy funds. Also as discussed below, creator funds win on deal sight and access, even if they lose on diligence - in this market following hot rounds is near enough a good strategy.

SEIS/Tax efficient funds (in the UK) - their deals are rarely exciting, but they need to return 0.3x for you to be in profit so the punt seems worth it.

Here’s what I look for when I review a fund deck

·Macro - are they investing into a macro trend that you believe in (i.e. is the sector growing or expected to grow fast according to you)

On thesis - do they make a thesis and stick to it / is there consistency in their portfolio or do they just spray and pray?

Think about region too here (also currency risk)

Micro - have they got a good deal by deal track record

Three parts to being a good VC: Sight, access and diligence

(You want to make sure that a fund achieves 2 out of these 3)

Sight: = do they see a lot of good deal flow

Access = what proportion of deals that they seen do they win - do they have a right to win deals that others don’t

Based on ticket size relative to value add (also visible by track record)

This can be done because they are a large fund and have a great reputation so can win rounds or if need be slightly outbid

Or better if they’re a small fund with extreme value add so they get into lots of deals

Diligence = can they tell good deal from bad. Do they have the ability to identify opportunities where others do not

This helps as you can get into rounds others do not believe in (and therefore get in at lower rates)

This also helps as you’ll have fewer misses

Specific things:

GP contribution = apart from for first time managers, this should be >5%, if not the skin in the game isn’t the same and they can be incentivised by the management fees

Fees = 2:20 as standard over a 10 year fund cycle

1x minimum before carry is split = better if there is an 8% a year hurdle or the like

Other stuff:

Best funds:

Imo = the best funds are small funds, emerging (first-time) managers with deep expertise in a specific area, as they can tag into good deals and are accessible to institutional investors

If you can get access then large funds that lead good rounds, but really here we mean Sequoia, Founder Fund, A16Z, Lightspeed, Bessemer and not many beyond that

Deck = if you can’t explain it simply, then you haven’t really understood

Anything too complex likely doesn’t make sense - a good fund manger will save that for the pitch

Team

Show don’t tell = what is your overall angel track record - not just a few winners

Have you built a good company before or learnt the ropes somewhere good

Do I sit in a room with you and get impressed - are you formidable https://paulgraham.com/convince.html)

Do they have bullshit jobs in their fund?

Does the team look meritocratic - are they properly incentivised?

Are the team by any metric super good - talent attracts talent and founders - if they team aren’t epic, their deal flow will be mid

Do not fall for experience - Venture fund partners who’ve already made their cash can often take up too much of the profit for doing none of the work, disincentivising the whole team (even if the team is overpaid, they will only look at their pay relative to the other people in the team and respective workloads)

Other LPs - can be a good indicator, but don’t let it be the guiding force

Strategy / number of deals:

They should be able to articulate a simple and sensible strategy that goes through sight, access and diligence so you can understand where they are on each

They should be doing (in my view 60 deals

Across 4 years - longer is likely better - remember you’re making an annual commitment for a set period of time as opposed to a lump sum commitment

Risk appetite - in all cases, higher risk also correlates to higher potential reward

Stage - early stage is riskier

Number of deals - fewer deals = more risk

Timeframe = short is risky - for this one I’d actually ensure a 4 year minimum investment period to prevent getting tucked into bubbles

Government support

If there’s Government money that matches or backs up your money (e.g. EIS/SEIS) then that can hugely amplify returns - would generally always do these funds)

Friends

I find with close (real) friends they won’t take your money unless they’re serious. I’ve never lost money investing in a friend (even when I didn’t believe in their company) - and I’ve only done it twice, but those are my top 2 portico’s - which probably says a lot

Note

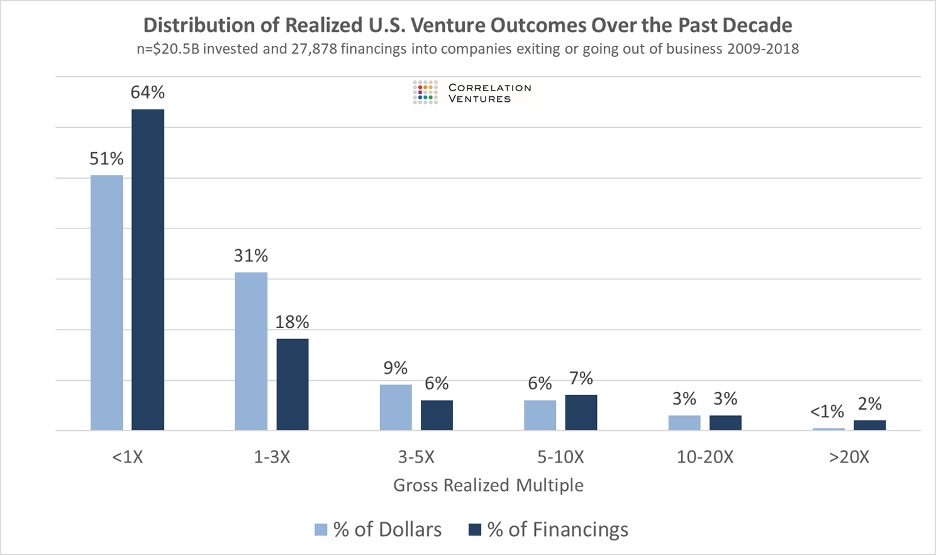

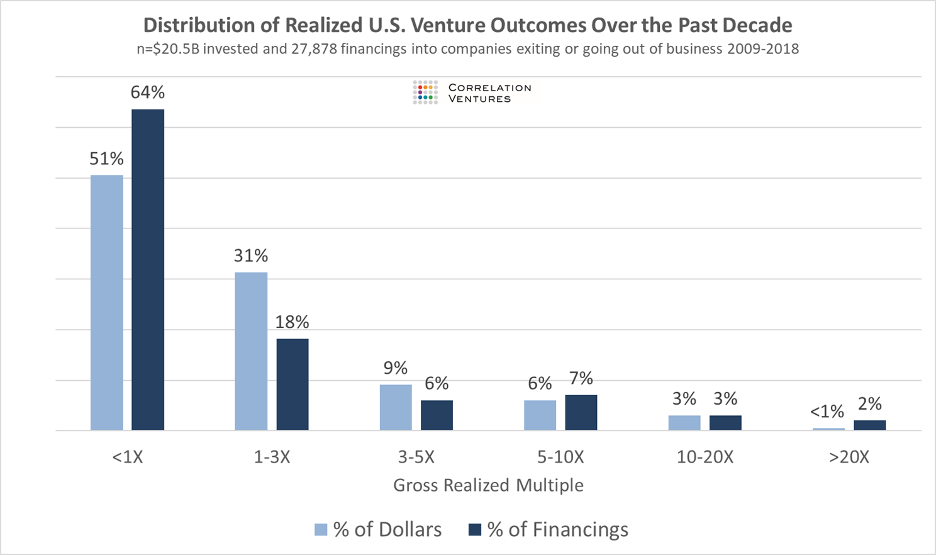

VC is all about outsized returns - so if your fund is not top quartile you’re in effect losing money - so really think about if the fund is top quartile on a combination of the 3 factors I raised earlier - sight, access, diligence