Why Runna won out: vibes and obsession

I had a view of Runna from day -100 to exit and turned a tiny investment into more than I'd saved throughout my time at McKinsey- here's why I think they won

I ramble in this piece, it’s a passion project, and I remember hearing first hand how hard that first raise was… so I start with a TLDR:

Every VC that passed overindexed on TAM, competitor threat and the lack of an engineer as a founder. all massively under indexed on how individually exceptional (as humans) the team were.

The team ran fast and hired people who were both running obsessed and had built similar functions before, as opposed to brand names on CVs.

SEIS is a gold mine that has massively inflated the returns early investors received by close to 4x… get in!

Venture is hard: Eka got solid terms on what was an entirely uncompetitive deal for them, this is the breakout success that most VCs can only dream of, yet it’ll likely only generate them 25x (based on the Times’s 30x estimate), which barely covers half of their fund. That said for everyone one of these deals they score, they can afford to have 8 fails and still 3x the fund. So you can decide whether picking startups is hard. That said, keep a close eye on the creator ventures strategy of passing on first rounds and getting in as they see traction, and doing 5-6x in 1.5 years.

Some from the sidelines say the founders sold early, that American VCs or founders would rarely have taken an exit when they had all the momentum. There may be truth to this, but those people are usually on the sidelines for a reason, and most of them passed on the deal… so… they can try to give this argument more weight when they too build and sell a company for 9-figures.

One of the most amazing things about Runna, is how in awe literally everyone at the company is at every new tier of success that they achieve.

From first round, to Forbes, to the acquisition, they’ve lived this business like kids in a candy store - a profitable one too.

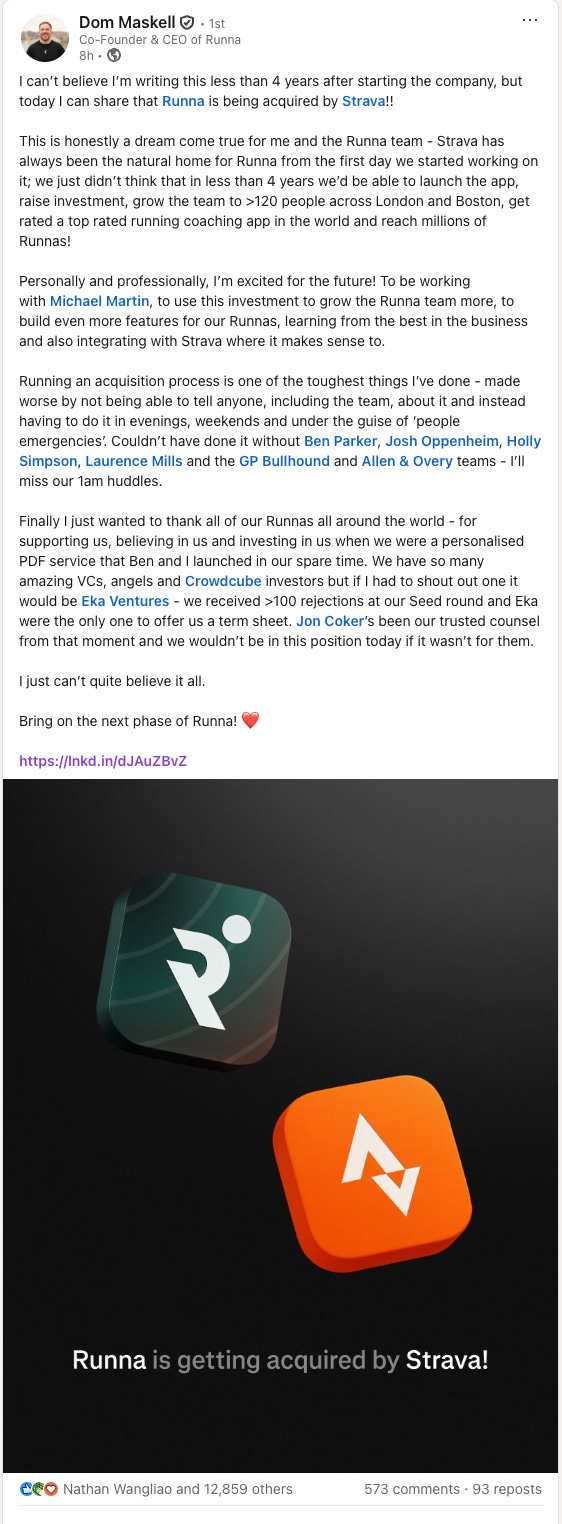

DREAM COME TRUE 🥺 best 4 years of my life, bring on the next 4 🫶

- Dom’s Instagram Comment on Strava’s post

First intros

I first properly got to know Dom, the running obsessed founder of Runna, when I was interviewing to move to his product team at McKinsey. I left with little view other than, he’s great vibes, and would be fun to work with. At the time I was deciding between working in his product team, or doing a secondment to McKinsey in Japan, and he very openly made his case for why being the first member of his team would be great, especially as a precursor to founding; but he was also clear that there was no pressure to take the role given that a secondment in Japan sounds pretty epic - I ended up doing neither, but the person who went to Japan in my place met the partner of their dreams and has moved their permanently so…

Discovery and first round

Months later, I saw on LinkedIn that Dom had left the firm (as we call it) to found so I dropped him a LinkedIn messaging offering to help in any way needed, later sending across VCs and Angels for him to speak too.

Of everyone I pointed out or sent the deal too, only one invested, a well know Partner at McKinsey who put in a £50k cheque that based on public estimates he’s 30x’d (but note due to SEIS he’s actually 109x’d his max loss), all capital gains free.

Everyone else passed. A friend who runs a well reputed fund in London refers to how this was one of his few major misses, as the founders had the optimal backgrounds according to their founder profiling methods.

In Dom’s LinkedIn post announcing the deal he refers to how they pitched 100 VCs and they received 1 term sheet.

There were several reasons for this (in my view):

Dom didn’t have the excessive public overconfidence (public school arrogance) that VCs love - he instead has an insane work ethic and great management style

The founding team had a running coach (albeit a tier 1 running coach) and a product CEO. Not the classic CEO CTO grouping. VCs as much as they say they back rebels, love patterns. Even VCs who talks about how they break the mould will assess based on a similar people model.

In hindsight, this CEO and expert/creator/specialist combo seems like it should be the go-to app model in a world where tech is becoming increasingly commoditised.

What’s also crazy is how many of these consumer apps were first built by dev shops after they were thought up by non-technical founders: Uber ($156bn), Linktree ($1.3bn), Calendly ($3bn)

Nobody believed in the potential market for the business. In some ways it felt like 2 school friends building an app - and almost all mobile apps fail. It didn’t feel like a VC backable business (more on this at the end)

Even when I invested it was purely in wanting to support a friend and founder who I rated, to this day I haven’t claimed any of the run plans or rewards that the crowd fund investors received. I hate running. I had no way to evaluate and no conception of a running app, but Dom was vibes, so I went in. In my existing angel track record, the only companies that have delivered solid consistent returns have been the friend cheques, and also the athletes - people who grind through the sh*t to get to the gold. The other one namely Chris Kong of Better Nature. I invested there 6-7 years ago, and he’s still going strong through all the sh*t that is running a consumer good startup.

Every VC I’ve spoken too since has said they underweighted the importance of the founder. If they’d just judged them on how exceptional they were as founders, the story would have been different. But it takes most to miss for one to win.

https://www.linkedin.com/feed/update/urn:li:activity:7318505721640189952/?commentUrn=urn%3Ali%3Acomment%3A(activity%3A7318505721640189952%2C7318510080021147648)&dashCommentUrn=urn%3Ali%3Afsd_comment%3A(7318510080021147648%2Curn%3Ali%3Aactivity%3A7318505721640189952)

That winner was, Eka Ventures who led the £1.9m seed round at around £6m pre-money valuation (based on backsolving). This happened the same quarter where I recall Runna was already doing strong monthly recurring revenue. None of the major funds went into the deal and the angel list was primarily creator focused.

Scaling and Series A

As the company scaled at an INSANE pace, I remember seeing the hockeystick, churn numbers and everything else, they quickly hit an insane monthly growth rate and revenue number - which I’m not at mercy to disclose. They then raised the next round at an unbelievably attractive valuation (c.£5m at a c.£30m valuation).

At that point, I was scaling the most viral content studio in the world, from which we spun up a creator VC fund - JD ventures. Using the leverage of our studio we were one of a few creator funds who participated in this hugely oversubscribed round and were only able to get a quarter of our requested allocation given how in demand the round was.

We deployed >5% of our fund into this deal, and in the process have returned a large chunk of the entire fund within 1.5 years of this investment. As far as I recall, this deal was done via a DM by Julius to Dom, then a short call with our team, and a relatively quick whatsapp back and forth between myself and Dom to agree on allocation and get the deal closed - super fast.

This round, led by JamJar, was followed on by a several other funds including my favourite fund Creator Ventures and Sasha Kaletsky, who have a superb strategy of using creator pull to get into consumer rounds, and always seeing deals early and then watching them until their next rounds, picking the winners (as they have done with Runna, ElevenLabs, Praktika and I’m sure many more).

Hypergrowth: the value of obsession

After this round, I performed a magic show at the Runna summer party at Dom’s house, and again could see this familial vibe, running obsessed. Unlike most corporates or startups, the team all gelled like a family, and had a great time working and playing!

I later also performed at their Runna Ambassador away day, and left feeling nothing but an obsession that everyone around me had with running. As someone who never even filled the forms for the free run plan that investors were offered, I obviously didn’t fit, and left the dinner as soon as food was done as I wasn’t sure I couldn’t do another conversation about running: In the greatest way! This was another part of the secret sauce. EVERYONE being obsessed. Literally EVERYONE who worked there, or was in any way tangentially involved was obsessed with running.

People loooovveee running… like I’m doing 5ks on lunch break cos that’s just what people do here - [friend who recently joined at Runna]

Obsession trumps all. From what I recall, beyond being more than a 9-5, the company didn’t seem to have an intense 9/9/6 culture that they US startups pride themselves on, they did have truly obsessed teams working for the good of the company.

Hypergrowth: hiring obsessed specialists

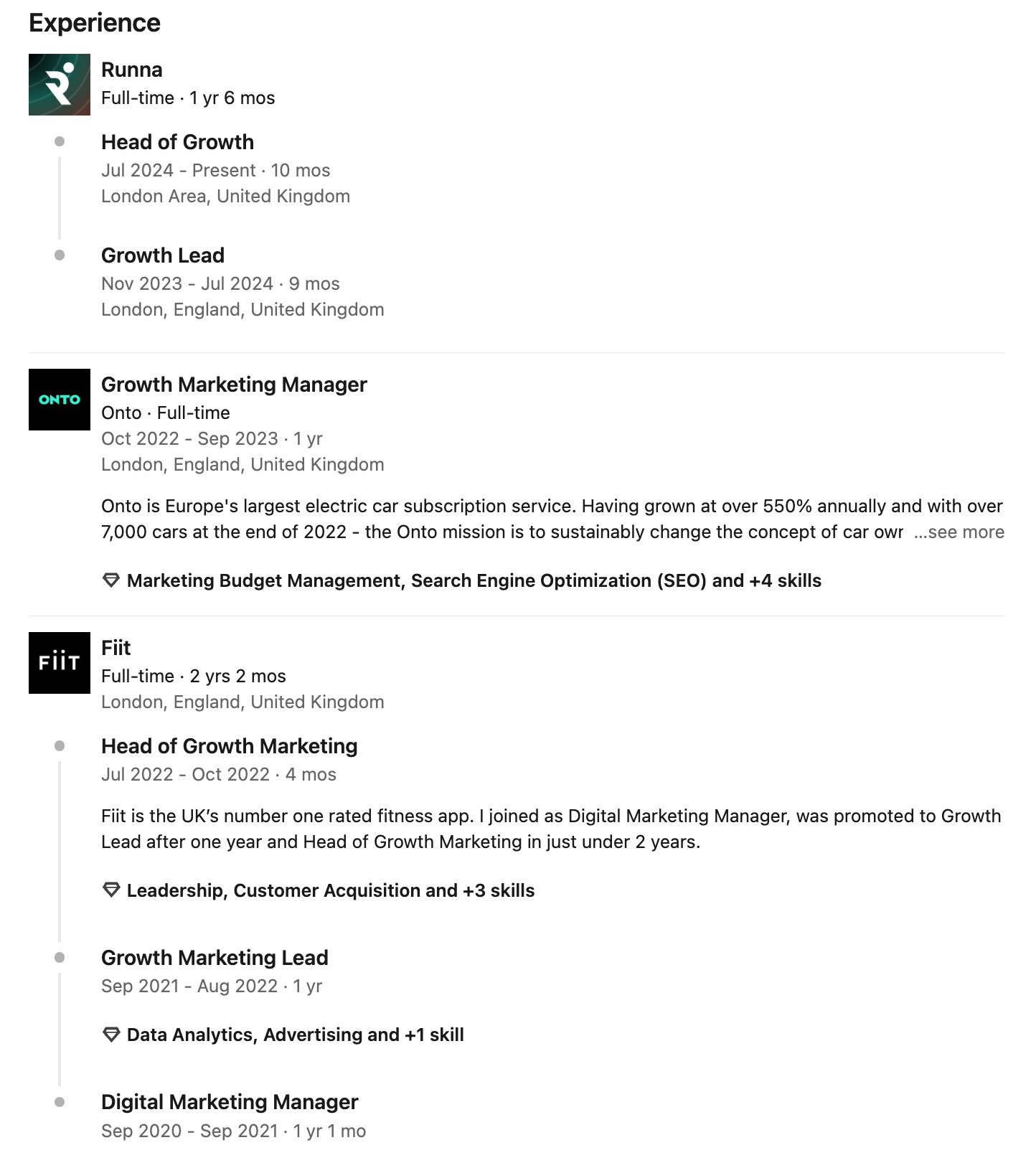

During this phase I’d often share vacancies with friends and at points considered applying myself. What I found was that they’d very quickly start hiring specialists, but specialists who were in some way obsessed with running - whether as beginners getting into it, or regular runners. Looking at their profiles, unlike Dom who was a generalist from a brand name firm, the majority of the rest did not come from large brand name organisations, but they’d built the same function at another org. This followed the classic Airbnb strategy of find people who’ve built the same product elsewhere and do whatever you can to hire them. Below is an example of a member of the growth team, who’d previously run a fitness app.

Start with the results and work backwards to the people.

Most people start with resumes, they start with brands, but you should actually ask yourself what products do I admire, and then who built those products, and who actually built them. It’s like a detective novel to find out who built them.- Brian Chesky (AirBnB CEO)

And then came the exit - and to nobodies surprise Strava went in… my tiny cheque has returned me more (tax free) gains than any money I saved during my years at McKinsey, and an given me an even better adventure.

What could have been

There is always going to be the other side of the acquisition where investors, the team, the spectators ask what could have been.

According to the Times, Runna returned c.30x to their earliest investors (to SEIS investors this was substantially higher but we’ll go with 30x). As one of the break out startup success stories in the UK, this investment won’t even be a fund returner for it’s largest investor shareholder.

It could be argued that if they had been in America, or had US investors on their cap table they may have not gone for an acquisition and instead try to outcompete Strava.

By the end of it, due to the level of dilution in their rounds, the founders held under 45% combined, maybe there was no incentive to take this further when they could sell and then get ready to do this all over again in a few years (this time raising at a crazy valuation from the get go).

To this I’d argue, “🤷”, two underestimated founders from the UK have just built from scratch (within 4 years) a company that has been acquired for 9-figures. Most people (including me) were just watching from the sidelines, it’s a fair point but not one many of us can dive into until someone offers us 9-figures for a company that was a mere idea 5 years ago.

Huge congrats to Dom, Ben and the entire team on this crazy adventure… onto the next part of it!

Note from me

I’ll be pretty actively deploying during this phase, so let me know if you either have an epic deal to pitch, or would like to angel invest and syndicate deals, please get in touch with me on LinkedIn.

I’ll be writing a tonne here, so please subscribe if you’re interested.